Europe's App Store Rules Are Rewriting Mobile Product Strategy

For years, mobile product strategy was shaped by a stable assumption: if you wanted scale on a phone, you built inside the App Store or Google Play and accepted the commercial terms as part of the job. The EU’s Digital Markets Act has started to weaken that assumption. What looked at first like a regulatory dispute is turning into something more operational for product teams: a new set of choices about payments, distribution, account relationships, and platform dependence.

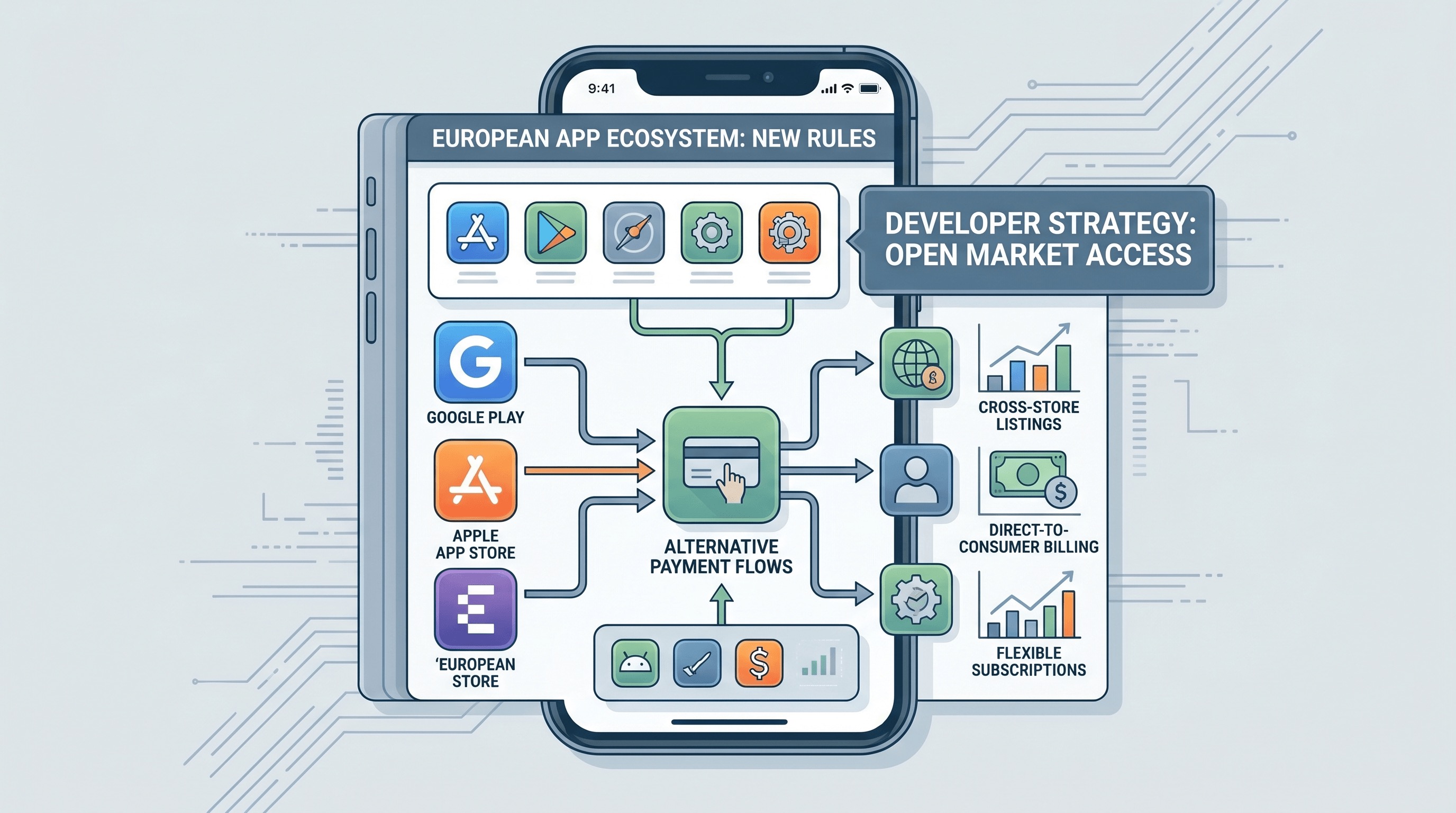

That is why the DMA matters far beyond Brussels. Apple now supports alternative distribution options, browser-engine flexibility, and more steering paths for offers in the EU, while Google has had to expand billing and external-offer options under similar competitive pressure. The result is not a sudden free market on mobile. It is a more fragmented but more strategic environment, where the product team has to decide which platform services are worth paying for and which customer relationships it wants to own directly.

This is really a monetization story

The public framing around the DMA often focuses on sideloading or alternative app stores, but the more immediate impact for many companies is monetization design. Once developers have more ways to steer users toward web checkout or alternative billing, pricing and onboarding stop being fixed by the platform. They become product decisions again.

That sounds liberating, but it also creates work. A team now has to think about whether the cleanest checkout lives inside the app, on the web, or in a hybrid flow that changes by geography. It has to model fee tradeoffs against conversion loss. It has to explain purchase history and subscription management when the same service may be sold through multiple routes. In other words, regulation is pushing mobile businesses to become more sophisticated retailers.

Alternative distribution is not automatically the main event

Alternative app marketplaces generate headlines because they sound dramatic. In practice, only some categories will benefit enough to justify the complexity. Games, high-margin subscriptions, and products with strong brand pull may have reasons to explore alternative distribution. Many ordinary apps will not. Discovery, updates, trust, and support are still real advantages when a platform handles them well.

That is the key strategic point. The DMA does not force every company to leave the default store path. It forces every company to evaluate what the default path is actually worth. For some, Apple or Google distribution will remain a sensible bundle of services. For others, the new rules create leverage: even if they never fully leave the store, they can now design around it more aggressively.

Mobile growth is becoming more web-aware again

One of the most interesting consequences is the return of the web as a first-class growth and billing surface. Mobile teams that had spent years optimizing around in-app purchase conventions are revisiting account-first onboarding, browser-based pricing pages, upgrade funnels, and retention programs that live outside the native app shell. That does not mean native apps matter less. It means the app is no longer assumed to be the whole business.

This shift also changes the economics of lifecycle marketing. If the platform no longer owns every critical transaction touchpoint, developers can build stronger direct relationships around offers, renewals, bundled plans, and customer support. That can improve margins, but it also raises the bar on operational discipline. Direct relationships are valuable precisely because you now have to maintain them yourself.

Geography is becoming part of product architecture

The DMA also creates a new kind of product complexity: regional product logic. A global app may need different payment flows, disclosures, default settings, or distribution mechanics depending on whether the user is in the EU. That breaks the old fantasy that mobile product design can be globally uniform apart from language and tax. Regulation is becoming part of interface design and revenue architecture.

Teams that already think this way will adapt faster. Payments, identity, trust prompts, legal copy, and analytics attribution all need to be designed as configurable systems rather than hard-coded assumptions. The mobile stack is getting more conditional, and companies that treat compliance as a product input instead of a last-minute review will be in a better position.

The platform still matters, just differently

None of this means platform power disappears. Apple still controls critical parts of the iPhone experience, from hardware integration to trust signals and security review. Google still benefits from default distribution and the practical inertia of the Play ecosystem. The DMA reduces absolute control, but it does not remove ecosystem gravity. That is why the real winners will not be the companies that simply celebrate “openness.” They will be the ones that make smart tradeoffs about when to use platform services and when to route around them.

There is also a user-experience trap here. Extra choice is not automatically better if the result is confusing subscriptions, inconsistent refund policies, or trust-eroding checkout handoffs. Product teams need to remember that a lower platform fee is only useful if users still convert and stay. Freedom without coherence can damage the business as easily as platform dependence can.

What mobile teams should do now

The practical move is to treat this moment as a strategy review, not a compliance patch. Map every user journey that touches purchase, renewal, upgrade, cancellation, and support. Decide which journeys belong inside the store and which are better owned directly. Build pricing and entitlement systems that can handle multiple acquisition paths. Revisit analytics so you can compare margin, churn, and conversion across those paths.

It is also worth investing in clearer account identity. The more distribution and billing options diversify, the more important it becomes that the user understands what they bought, where they bought it, and how support works. Good account architecture becomes part of trust.

The DMA is reshaping mobile in a subtle but durable way

The biggest effect of the DMA may not be a wave of alternative app stores. It may be the normalization of mobile product teams thinking like cross-channel commerce teams. Once pricing, distribution, and customer ownership are no longer fixed by a single platform rulebook, strategy gets more interesting and more demanding.

That is the real mobile story here. Europe’s app store rules are not just changing what is allowed. They are changing what competent product teams need to know. The future of mobile business looks a little less like platform obedience and a little more like channel design.

Actionable takeaways

If you ship a mobile product in Europe, run a margin-by-flow audit now. Compare in-app purchase, alternative billing, and web checkout with real conversion assumptions instead of ideology. Build region-aware entitlement logic before you need it. And if you are tempted to treat DMA changes as a legal side quest, resist that instinct. This is now core product strategy.