Why Startup Liquidity Is Moving to the Secondary Market

For years, the promise of a big IPO or acquisition was the golden ticket for startup employees. Their equity, often a significant portion of their compensation, was a long-term bet on the company's eventual public debut or sale. But the game has changed. Startups are staying private for much longer – a decade or more is no longer uncommon – and with that extended timeline comes a pressing question: How do employees access the value they’ve helped create before an exit event that might still be years away?

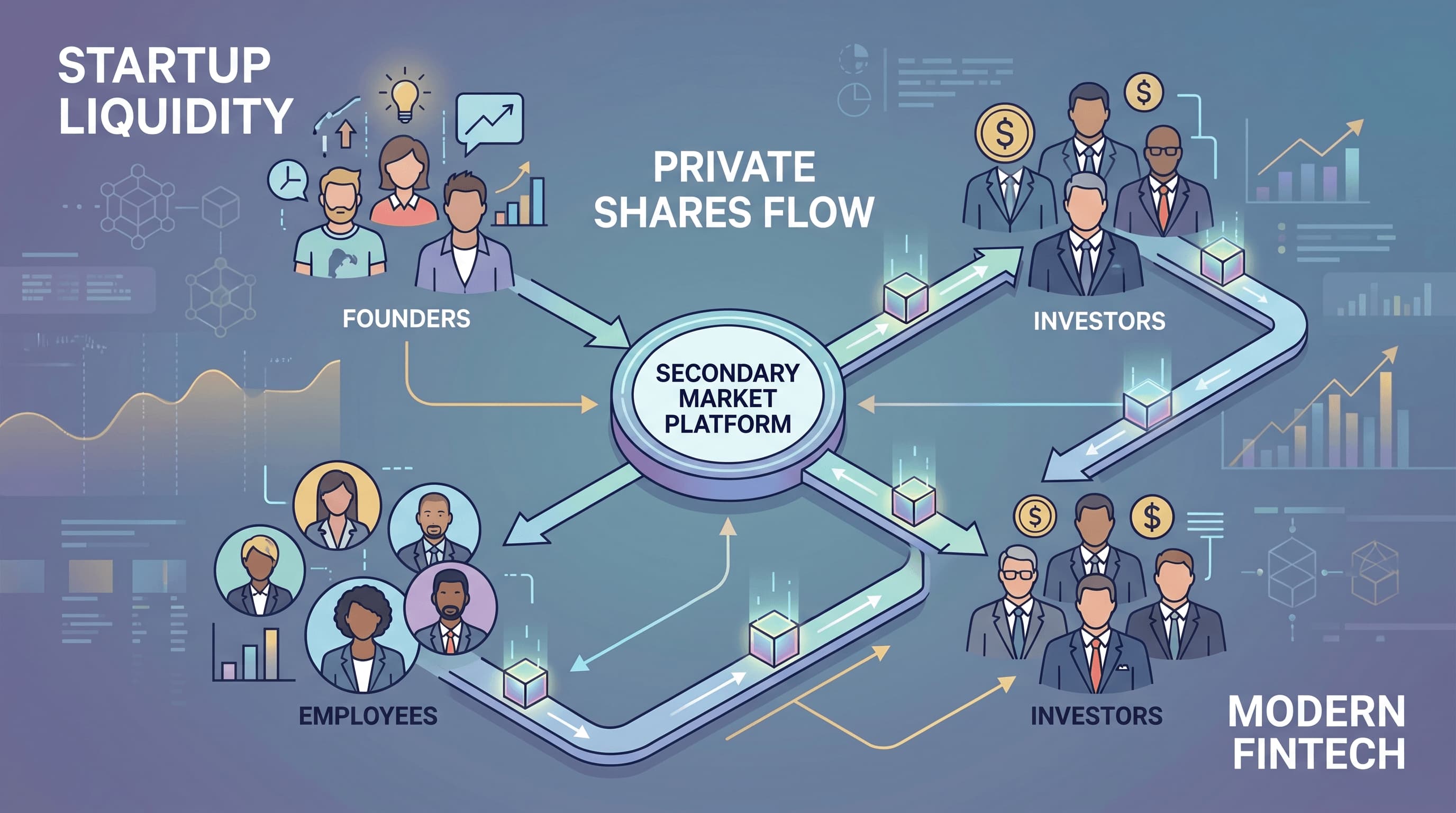

The answer, increasingly, lies in the secondary market. What was once a niche activity or a sign of distress is rapidly evolving into a normal, even essential, part of the private market infrastructure. Companies like Stripe and Rippling are leading the charge, demonstrating how structured liquidity programs are becoming crucial for talent retention and cap table management.

What Are Secondary Sales and Tender Offers?

Let's break down the jargon. When we talk about secondary sales in the context of private companies, we're referring to transactions where existing shareholders sell their shares to new buyers. Crucially, the company itself isn't issuing new shares; it's a transaction between two parties who already hold or want to hold company equity. Think of it like selling your used car – the car manufacturer isn't involved in that specific transaction.

A "tender offer," on the other hand, is a more formal, company-sponsored program. In a tender offer, the company (or a lead investor) offers to buy back shares from a specific group of shareholders – often current and former employees – at a pre-determined price within a set timeframe. It's a structured event, typically approved by the board, designed to provide liquidity in a controlled manner. It’s less like selling your car to a random buyer and more like the car manufacturer offering to buy back a specific model from owners for a limited period.

Why Employees Are Driving This Shift

The motivation for employees is straightforward: life happens. While a startup’s equity can be incredibly valuable, it remains "paper rich" until an IPO or acquisition. Employees have mortgages to pay, children to educate, unexpected medical expenses, or simply want to diversify their personal wealth. Waiting 10-15 years for an IPO means their compensation, a significant portion of which is often in equity, is locked up indefinitely. This creates "golden handcuffs" that can eventually chafe, leading to burnout or a desire to move to a public company where their compensation is immediately liquid.

Providing a mechanism for employees to realize some value from their equity, even if it's a fraction of their holdings, can be a massive morale booster and a powerful retention tool. It acknowledges their contribution and helps them manage their personal finances without having to leave the company.

Why Founders and Boards Can't Afford to Ignore It

For founders and boards, secondary liquidity isn't just about employee happiness; it's a strategic imperative. Ignoring the need for liquidity can have severe consequences, from talent drain to complicated cap tables. Here's why they don't treat these transactions casually:

Valuation Management

Any sale of shares, especially a tender offer, sets a price point for the company's equity. This valuation needs to align with the company's strategic goals, future fundraising plans, and internal assessments. An uncontrolled secondary market where shares trade at wildly different or unexpectedly low prices can complicate future funding rounds and create perception issues. Tender offers, being company-controlled, allow the board to set a price that reflects their current valuation expectations.

Cap Table Health

A "clean" capitalization table (cap table) is vital for future investors and eventual public listing. Uncontrolled secondary sales can fragment ownership, introducing numerous small, potentially unsophisticated shareholders who might complicate governance or future transactions. Tender offers can be designed to consolidate ownership or manage the number of shareholders, ensuring the cap table remains manageable and attractive to institutional investors.

Talent Retention and Acquisition

In today's competitive tech landscape, offering competitive equity compensation isn't enough; offering liquid equity compensation is becoming the differentiator. Companies that provide controlled liquidity options signal to prospective and current employees that they are committed to their financial well-being. This can be a powerful tool for attracting top talent who might otherwise gravitate towards public companies or startups with clearer exit paths.

Strategic Delay of IPOs

The ability to provide liquidity without going public allows companies to stay private longer. This means they can continue to focus on long-term growth, product development, and market expansion without the quarterly pressures and regulatory burdens of the public markets. It gives them more control over their narrative and allows them to mature fully before facing public scrutiny.

The Data Speaks: Secondary Markets as Normal Infrastructure

The shift is evident. Both Nasdaq Private Market and Carta, key players in the private market ecosystem, have highlighted the increasing importance of tender offers and secondary sales. Their observations confirm that companies are indeed staying private longer, making employee liquidity a critical need before an IPO.

Consider recent examples: Stripe, a fintech giant, announced a significant 2025 tender offer for its current and former employees, allowing them to sell shares at a robust $159 billion valuation. Similarly, Rippling, a fast-growing HR and IT platform, secured $450 million in new financing and simultaneously arranged to repurchase up to $200 million of employee equity at a $16.8 billion valuation. These aren't isolated incidents; they are symptomatic of a broader trend.

Carta's data from 2025 further reinforces this. They reported strong participation in tender offers, with later-stage companies driving most of the activity on their platform. This isn't just an emergency measure for companies in distress; it's becoming a standard piece of the financial infrastructure for successful, maturing private companies.

Navigating the Risks and Challenges

While secondary markets offer significant benefits, they are not without their complexities and risks. Founders, employees, and investors need to be aware of these:

Pricing Opacity and Fairness

Determining a fair price for private company shares can be challenging. Unlike public markets with transparent, real-time trading, private valuations are often less clear. In secondary sales, there can be significant information asymmetry: buyers (often sophisticated institutional investors) may have access to more detailed financial information or market insights than individual sellers (employees). While tender offers aim to mitigate this by setting a board-approved price, questions can still arise about how that valuation was reached and if it truly reflects the company's potential.

Access and Eligibility

Not all employees may be eligible to participate in a tender offer, or the amount they can sell might be capped. Eligibility often depends on factors like vesting schedules, tenure, role, or even the amount of equity held. This can create a sense of unfairness or division among the workforce if some are granted liquidity options while others are not.

Information Asymmetry

This is a persistent challenge in private markets. Employees selling shares often lack the full picture of the company's financial health, strategic roadmap, or potential future fundraising rounds that buyers or the company itself might possess. This imbalance of information can lead to sellers potentially underselling their equity.

Uneven Eligibility

As mentioned, the criteria for participation in tender offers can vary widely. Some programs might prioritize long-tenured employees, others might focus on early hires, and some might be open to all vested employees up to a certain percentage of their holdings. Managing these expectations and ensuring perceived fairness is a delicate balance for companies.

The Quiet Revolution: A New Liquidity Layer

The core thesis holds true: the private market is quietly but surely building its own sophisticated liquidity layer. This isn't just about employees getting paid; it fundamentally reshapes how startups operate:

- Talent Retention: Equity compensation becomes a more tangible, less abstract benefit, allowing companies to compete more effectively for talent against public market giants.

- Cap Table Management: Boards gain a proactive tool to manage their shareholder base, preventing fragmentation and ensuring strategic alignment.

- IPO Timing: Companies have greater flexibility to delay their public debut, allowing them to mature, scale, and achieve their strategic goals without external pressure to go public prematurely.

This evolution signifies a maturing of the private market. What began as an informal workaround is now becoming an institutionalized practice, changing the very definition of success and sustainability for high-growth startups. As this trend continues, we can expect even more innovative solutions to emerge, further blurring the lines between private and public market liquidity.