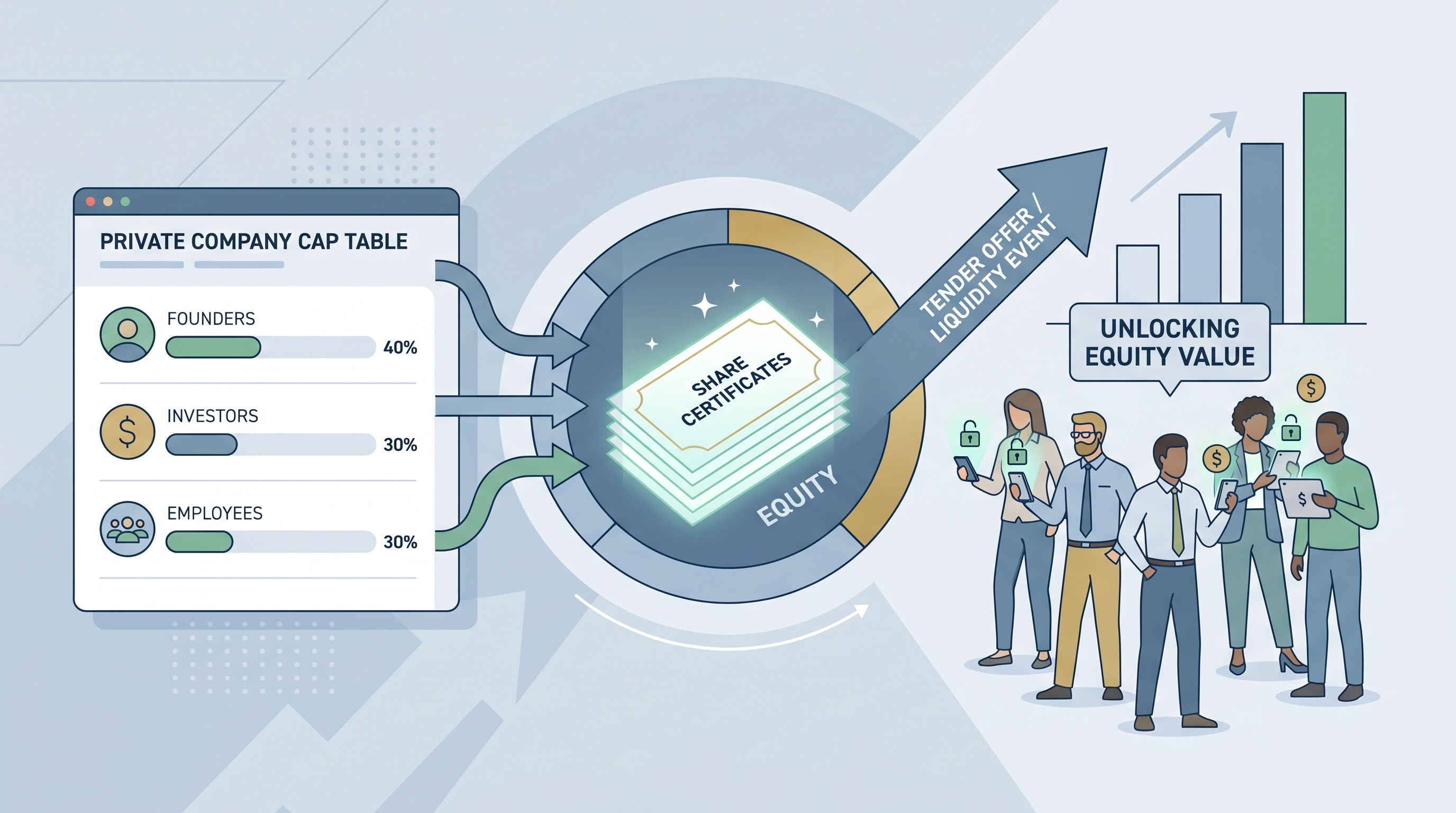

Tender Offers Are Rewriting the Startup Liquidity Timeline

The startup exit story used to have a cleaner arc. A company raised a few rounds, handed employees stock options, scaled aggressively, then aimed for an acquisition or IPO within a timeframe that felt vaguely human. That timeline has broken down. Startups now stay private longer, late-stage valuations can float for years without a public listing, and employees are increasingly asked to treat illiquid equity as compensation while waiting for an exit that may keep moving. Tender offers are emerging as the practical answer to that mismatch.

The important point is not just that more private companies are running them. It is that tender offers are changing what startup liquidity means. They are turning liquidity from a single finish-line event into a managed company function, somewhere between compensation policy, cap-table strategy, and talent retention. That shift has consequences for founders, investors, and especially employees who have spent years being paid partly in paper wealth.

Private markets stretched the old bargain too far

For a long time, the social contract at a venture-backed startup was easy to summarize: take below-market risk now, get upside later. That logic weakens when later becomes ten or twelve years away. According to private-market research repeatedly cited across 2025 and 2026, companies are staying private far longer than they did a decade ago. The IPO window has reopened in fits and starts, but not enough to restore the old assumption that employees can simply wait for public-market liquidity.

That delay creates a structural problem. Equity still plays a central role in recruiting, but its motivational power erodes if workers cannot convert any of it into cash on a reasonable timeline. A senior engineer who joined in year two may now be in year nine, juggling taxes, option exercise decisions, and life choices around a liquidity event that keeps receding into the distance. At that point, “just wait for the IPO” stops sounding like upside and starts sounding like indefinite deferral.

This is why tender offers have become more common. They let a company, or sometimes an outside buyer working with the company, purchase shares from employees and early investors at a defined price. No, they are not a full exit. But they give people a way to realize some value without forcing a sale of the company itself.

Tender offers are becoming a normal operating tool

Recent Carta data cited in 2025 market summaries showed a sharp rebound in tender activity, especially among Series C and later companies. That fits what many founders and private-market advisors have been saying for a while: tender offers are no longer rare cleanup events for unusual cap tables. They are becoming a standard mechanism for mature private companies that need to retain talent, manage shareholder expectations, and prove that equity still means something.

That normalization matters. Once tender offers become part of the expected toolkit, they stop being interpreted as distress or pre-exit improvisation. Instead, they begin to function like compensation maintenance. A company can refresh morale, reduce pressure on long-tenured employees, and give recruits evidence that equity is not merely theoretical.

This is especially important in AI and other hot sectors where large private companies compete directly with public-market employers. If one employer can offer liquid stock and another can only offer a promise, the private company eventually needs a better answer than brand prestige. Tender offers are increasingly that answer.

Liquidity is now a retention product

The best way to understand the current shift is to stop thinking about tender offers purely as finance. They are also labor-market infrastructure. In a prolonged private-company cycle, partial liquidity is one of the few credible ways to keep early employees aligned without demanding endless patience.

That does not mean every employee should sell every share they can. In some cases, especially at companies still compounding rapidly, retaining meaningful upside makes sense. But the existence of a choice changes the relationship. It lets employees derisk a little, pay taxes, buy homes, or simply stop treating equity as an abstract number in a dashboard. That can make people more, not less, willing to stay.

There is a subtle management benefit too. Employees who have already realized some value often make calmer decisions than employees who feel trapped between hope and uncertainty. A partial sale can reduce the emotional volatility that accumulates when compensation is tied to a future transaction outside an individual’s control.

The secondary market is growing up around this demand

Tender offers are part of a larger shift in private-market liquidity. Secondary transactions, continuation vehicles, and structured private share sales have all expanded as investors search for ways to return capital without waiting for a classic exit wave. In other words, the market is building substitutes for the old IPO-centric path because the original path no longer clears often enough.

That growth is useful, but it also changes power dynamics. Secondary markets reward companies with strong demand and clean governance, while weaker firms may still struggle to create meaningful liquidity. Tender offers work best when management runs them deliberately, communicates clearly, and avoids turning them into insider-friendly events that benefit only a narrow circle. If the company wants employees to treat the program as trust-building, it has to behave that way.

Pricing is central here. A tender offer price sends a signal, even when it is imperfect. If employees believe the price reflects real conviction and fair process, the event can strengthen confidence. If they believe the price is overly managed or selectively available, the same event can breed cynicism.

Tender offers do not replace exits, and that is the point

Some investors worry that widespread private liquidity could reduce pressure to go public. There is some truth in that. If companies can raise large rounds, sell secondary shares, and offer periodic tenders, the urgency around IPO timing decreases. But that is not necessarily unhealthy. One reason the old exit culture produced bad outcomes is that it pushed companies toward liquidity milestones before their businesses or market conditions were ready.

A better framework is to treat tender offers as pressure valves. They help private companies stay private for the right reasons rather than because everyone is trapped. That distinction matters. A company with credible internal liquidity options has more strategic freedom than one whose cap table is effectively held hostage by employee impatience.

That said, tender offers are not a magic solution. They do not simplify tax rules, eliminate valuation risk, or guarantee future liquidity. They can also expose difficult internal questions about who gets to sell, how much, and at what cadence. Once a company runs one successful tender, employees may reasonably expect another. Liquidity, like compensation, tends to become part of the baseline once introduced.

What founders should learn from the trend

The broader lesson is that startup finance is becoming more employee-aware. Not kinder, exactly, but more realistic. Founders can no longer assume that mission and upside will carry teams through an extended private lifecycle without periodic proof that the upside is tangible.

That means liquidity planning deserves earlier attention. If a company expects to stay private into late stage growth, it should think about tender programs the way it thinks about refresh grants, compensation bands, and executive hiring. Not as an emergency measure, but as part of a durable operating model.

It also means founders should be honest about what equity can and cannot promise. The old mythology treated startup stock as a lottery ticket with an almost moral certainty of payout if everyone worked hard enough. The real picture is messier. Tender offers are one sign that the market is adapting to that reality.

The startup timeline has already changed

The rise of tender offers does not mean IPOs are dead or that acquisitions matter less. It means the once-dominant assumption of a single liquidity climax no longer matches how modern startups actually mature. The private lifecycle is longer, the cap table is more complex, and employees need something more credible than perpetual anticipation.

That is why tender offers matter beyond their legal structure. They acknowledge that liquidity is not just an investor concern. It is a company-design problem. And the startups that handle it well will have an advantage, because in a market where everyone offers equity, the ability to make that equity usable is becoming a differentiator.

The new startup bargain is not upside later. It is upside, managed over time.