Stablecoin Settlement Is Pulling Cryptocurrency Into Mainstream Payments

Cryptocurrency has spent much of the past decade arguing about ideology, speculation, and the future of money. Stablecoins are forcing a more practical conversation. They are less flashy than volatile tokens and less culturally loud than crypto’s early retail cycles, but they may end up being the sector’s most important bridge into mainstream finance.

The reason is simple. Stablecoins do something banks, fintechs, and global businesses immediately understand: they move dollar-denominated value quickly, globally, and in programmable form. That alone does not guarantee mass adoption. Regulation, reserves, compliance, and distribution still matter enormously. But in 2026, stablecoins are no longer just crypto plumbing. They are starting to look like payments infrastructure.

Why stablecoins are getting traction now

Timing matters. The early stablecoin pitch was often strongest in crypto-native markets where traders needed a dollar proxy or DeFi users needed collateral that did not swing wildly in value. That use case was real, but narrow. What has changed is that larger institutions now see stablecoins as a settlement tool rather than as a speculative product.

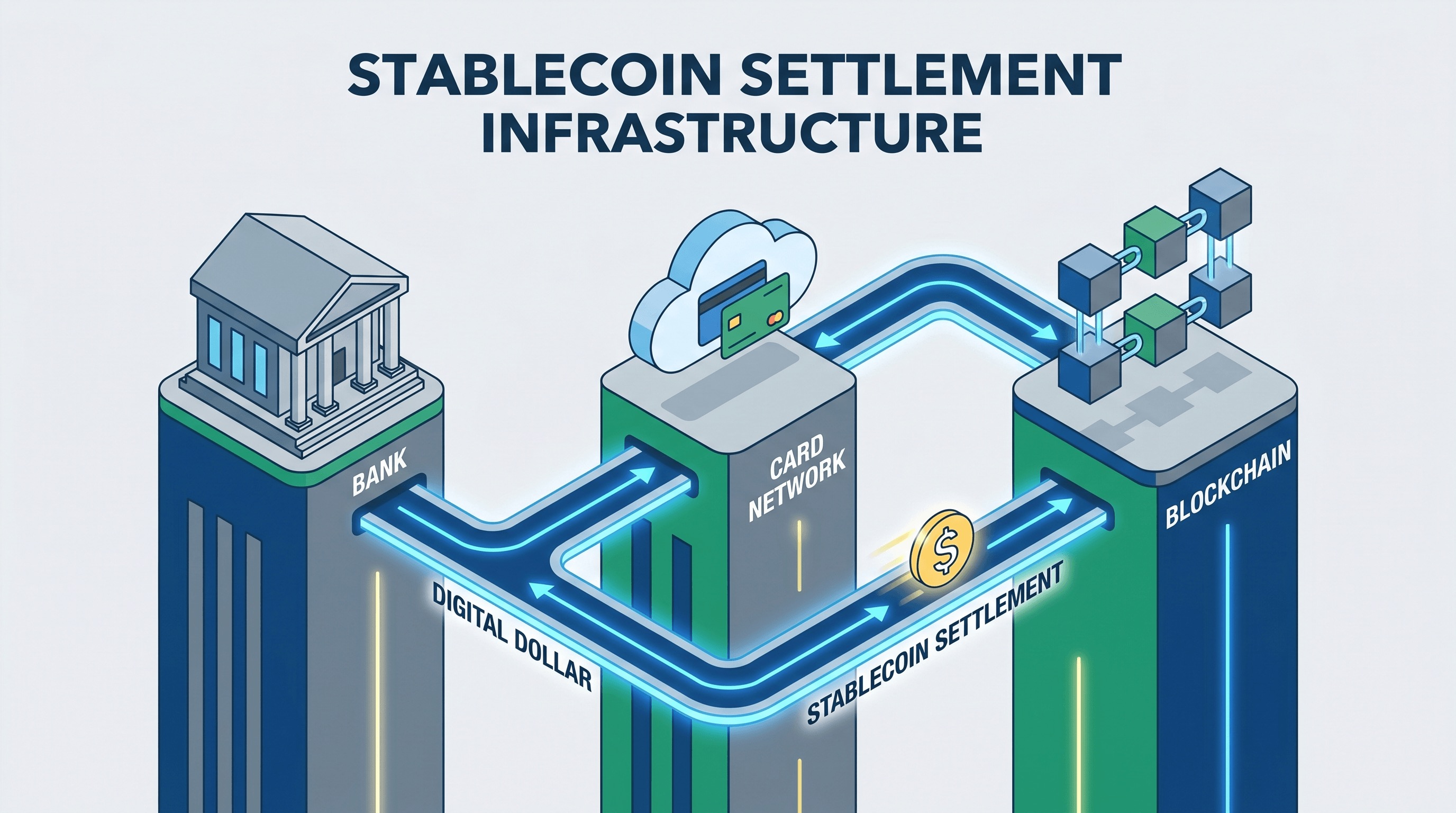

Visa’s December 2025 announcement that it was launching USDC settlement for U.S. issuers and acquirers made that shift harder to dismiss. The headline was not about replacing cards with crypto. It was about upgrading the back-end settlement layer while keeping the consumer experience intact. Visa framed the appeal in operational language: faster funds movement, seven-day availability, and more flexible treasury management. That is exactly the vocabulary mainstream finance uses when a technology starts becoming serious.

Stripe has been moving in the same direction from another angle. Its recent stablecoin strategy is about enabling businesses to accept, hold, and pay out value across borders with fewer intermediaries. The attraction here is not philosophical decentralization. It is practical settlement. Cross-border money movement remains expensive, slow, and often fragmented by local banking constraints. Stablecoins offer a software-shaped alternative that can fit into internet-native workflows more easily than legacy rails.

This is not the same as mass consumer crypto payments

One common misunderstanding is to treat stablecoin growth as proof that people suddenly want to buy coffee by scanning a Wallet. That may happen in some markets, but it is not the main story. The more important opportunity is back-end movement of funds: merchant settlement, treasury transfers, global contractor payouts, marketplace disbursements, and cross-border B2B flows.

That distinction matters because it explains why stablecoins can succeed even if average consumers barely notice them. Many infrastructure technologies work this way. The winner is not always the one that changes user behavior directly. It is often the one that removes friction underneath existing products. Stablecoins are increasingly being evaluated in those terms.

Regulation is turning from blocker to filter

Regulation has long been the biggest brake on institutional stablecoin adoption, and for good reason. If a dollar-denominated token is going to act like settlement infrastructure, then reserve quality, redemption rights, compliance obligations, and legal clarity cannot be vague. The market learned that lesson the hard way from poorly designed or poorly governed stablecoin experiments.

What is different now is that regulation is beginning to function less as a universal blocker and more as a market filter. Frameworks such as MiCA in Europe and new U.S. policy momentum around payment stablecoins are helping define which issuers look credible enough for enterprise use. That does not eliminate risk, but it changes the conversation from whether stablecoins can be used at all to which stablecoins, under which rules, for which counterparties.

The banking question is getting sharper

Stablecoins also force banks into an awkward but important strategic choice. They can treat tokenized dollars as a peripheral crypto curiosity, or they can treat them as a new interface for money movement that may eventually sit alongside cards, wires, ACH, and local payment rails. The second view is becoming harder to ignore.

That does not mean banks vanish. In fact, stablecoin settlement may work best when banks, networks, and regulated issuers cooperate. Banks still matter for custody, compliance, liquidity, customer relationships, and integration with the rest of the financial system. But the stack changes. Money movement starts to look more continuous, more programmable, and more global by default.

What could still go wrong

None of this guarantees a clean rise. Stablecoin infrastructure is still exposed to blockchain congestion, issuer concentration, regulatory reversals, and uneven integration with local finance rules. A payment system only becomes infrastructure when reliability becomes boring. Stablecoins are not fully there yet.

There is also a governance problem. If stablecoin power consolidates around a small set of issuers, chains, and distributors, the system may end up looking less open than crypto advocates imagined. That may still be commercially successful, but it would change the political meaning of the technology.

Why this trend matters anyway

Even with those caveats, the direction is striking. The most credible path for cryptocurrency into the economic mainstream may not be through speculative assets becoming everyday money. It may be through stablecoins becoming a settlement layer that other financial products quietly rely on. That is a more modest story, but it is also a more believable one.

When a technology stops asking users to change their identity and starts helping institutions solve a cost, timing, or liquidity problem, adoption usually accelerates. Stablecoins appear to be entering that phase. They are not replacing finance. They are starting to seep into it.

That is why this moment matters. Stablecoin settlement is pulling cryptocurrency out of the world of edge-case enthusiasm and into the slower, harder, more consequential world of real infrastructure. If that continues, the biggest crypto success story of this cycle may look less like a token rally and more like a treasury software upgrade.