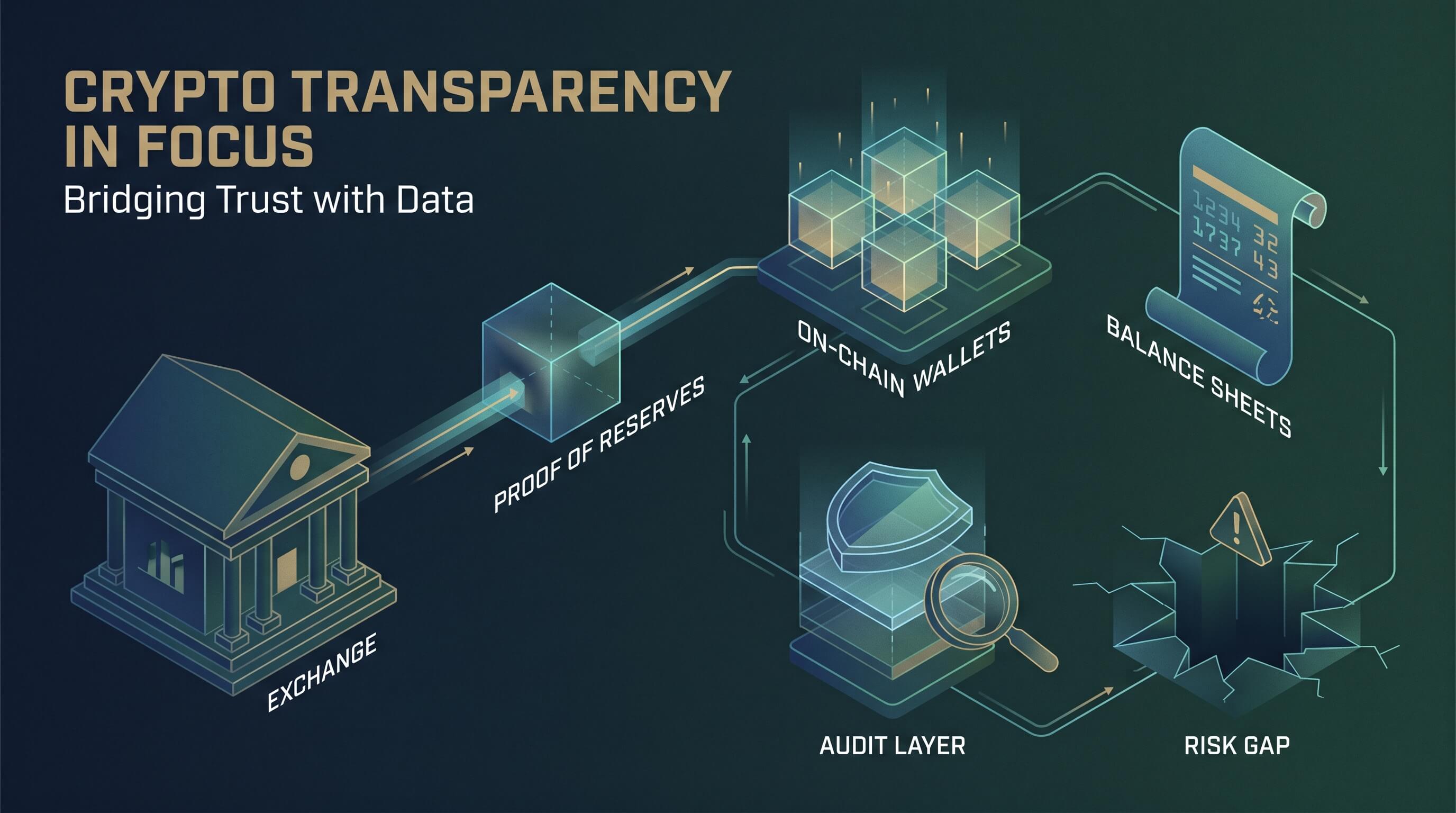

Proof of Reserves Still Does Not Prove an Exchange Is Safe

Proof of reserves became one of crypto’s favorite trust signals after the collapse of FTX, and that shift made sense. If an exchange can cryptographically show that it controls a set of on-chain assets, that is better than asking customers to trust a black box. But the stronger claim that often follows, that proof of reserves means an exchange is safe, does not hold up. Proof of reserves is useful transparency. It is not a full solvency test, a governance audit, or a guarantee that customer funds are protected from misuse.

The core thesis is simple. Proof of reserves can help answer one question, whether an exchange appears to hold certain assets at a specific moment. It does not answer several harder questions that matter just as much: what the exchange owes outside customer balances, whether liabilities are complete, whether assets are encumbered, whether insiders can move funds after the snapshot, or whether risk controls are strong enough to survive stress. Readers should treat proof of reserves as one input in a broader due-diligence process, not as a verdict.

What proof of reserves actually proves

In most implementations, an exchange publishes wallet addresses or signs messages from them to show control over assets, then works with an auditor or attestation firm to compare those assets against a snapshot of customer liabilities. Many systems use a Merkle tree so users can verify that their own account balance was included in the liability set without exposing everyone else’s data.

That matters. If an exchange can demonstrate that it controls enough Bitcoin, Ether, or stablecoins to cover customer deposits in the snapshot, that is materially better than a pure promise. It reduces one category of opacity. It may also make it harder for an exchange to claim reserves that do not exist on-chain.

But even a well-implemented Merkle-tree attestation is narrower than many users assume. It is usually an attestation at a point in time, not a live feed. It typically focuses on selected assets, not the full balance sheet. And it depends on the scope of the engagement, the integrity of the underlying records, and the exchange’s willingness to disclose all relevant obligations.

A reserve snapshot is not the same as continuous solvency

The biggest limitation is timing. A proof-of-reserves report is usually a snapshot. An exchange may look healthy at 10:00 a.m. on audit day and take on very different risk by 4:00 p.m. if funds can be moved, borrowed, pledged, or rehypothecated. That does not mean every exchange is gaming the process, but it does mean the result should be read for what it is: evidence about a moment, not a permanent state.

A practical example makes the point. Imagine Exchange A shows $5 billion in customer assets on-chain and $4.8 billion in customer liabilities in its Merkle tree. On paper that looks reassuring. But if part of those reserves came from a short-term loan arranged around the audit window, or if the exchange later transfers collateral to support proprietary trading, the attestation did not protect customers. It only described a temporary picture.

Frequency helps, but it does not solve everything

More frequent attestations are better than annual or sporadic ones. Daily or near-real-time proofs reduce the room for window dressing. Still, frequency cannot fix a report that excludes key liabilities or ignores governance failures. A bad business with frequent snapshots can remain a bad business.

Proof of reserves does not reveal the whole liability side

This is where many crypto discussions become too generous. Reserves are only one half of the question. Safety depends on liabilities too. If an exchange owes customers one amount, owes lenders another amount, has made side agreements with affiliates, or has promised collateral elsewhere, then a narrow reserve proof can create false comfort.

Consider Exchange B. It publicly shows large on-chain reserves and publishes a polished dashboard. Users conclude that funds are fully backed. But the company may also have off-balance-sheet obligations, loans to related parties, legal claims, token-denominated liabilities that were omitted from the report, or guarantees made through affiliates. None of that is visible from reserve addresses alone.

This is why some critics prefer the broader term proof of solvency. In theory, that would combine verified assets with a fuller accounting of liabilities. In practice, even proof of solvency is hard to execute cleanly without strong accounting controls, independent oversight, and clear disclosure standards. Still, it points to the right principle: reserves without liabilities are incomplete.

Asset control does not equal good custody or governance

An exchange can control wallets and still be unsafe. The failure mode may be operational rather than accounting-based. Weak internal controls, poor key management, concentrated admin access, sloppy incident response, thin compliance teams, or aggressive related-party arrangements can all put customer assets at risk even if the reserve wallets are real.

Think about the difference between possession and protection. A company may indeed hold your coins today, yet still expose them to tomorrow’s disaster through fragile custody architecture or reckless treasury decisions. A proof-of-reserves page will not tell you whether the exchange requires multi-party approvals for transfers, segregates duties between trading and custody teams, or maintains credible policies for market stress and redemptions.

Security incidents bypass the attestation story

History offers plenty of examples where custody and security failures mattered more than marketing claims. If an exchange is hacked, if a hot-wallet policy is too loose, or if privileged insiders can override controls, customer risk rises immediately. Proof of reserves does not audit cyber resilience. It does not certify operational maturity.

What careful users should look for beyond proof of reserves

If you are evaluating a centralized exchange, start by treating proof of reserves as a minimum transparency feature, not a premium seal of safety. Then look for the harder signals.

First, ask whether liabilities are independently described in enough detail to be meaningful. Second, check whether the exchange discloses who performed the attestation, what standards were used, and what was excluded. Third, look for evidence of segregated customer assets, strong custody controls, and credible legal terms around asset ownership. Fourth, pay attention to jurisdiction, licensing, enforcement history, and whether the company has a pattern of evasive communication during stress. Fifth, ask whether you actually need to keep assets on the exchange at all.

A practical rule helps here: if the exchange’s explanation of safety depends more on branding than on scope, methodology, and controls, your confidence should go down, not up. Good transparency is specific.

The right takeaway for crypto users

Proof of reserves is worth having. The industry is better off with verifiable wallet control, liability-inclusion tools like Merkle trees, and more pressure for public disclosure than it had during crypto’s least accountable years. But users should resist the urge to turn a useful tool into a comforting myth.

The right conclusion is not that proof of reserves is fake. The right conclusion is that it answers a narrow question well and leaves several existential questions unanswered. If you hold meaningful funds on a centralized platform, assume that safety depends on reserves, liabilities, custody design, governance, regulation, and your own habits. Use exchanges for liquidity and execution when you need them. Do not outsource all skepticism to a dashboard.

Actionable takeaways

Treat proof of reserves as a baseline transparency check, not a complete safety audit. Prefer exchanges that publish methodology, auditor identity, liability scope, and regular updates. Avoid keeping long-term holdings on platforms that cannot clearly explain custody and governance. When possible, move strategic holdings to self-custody or qualified custody solutions you understand. And if an exchange markets proof of reserves as the end of the conversation, treat that as a reason to ask more questions, not fewer.